The Reflexivity Problem with eHGV Residual Values

The Reflexivity Trap: Why eHGV Financing Is Stuck in a Loop

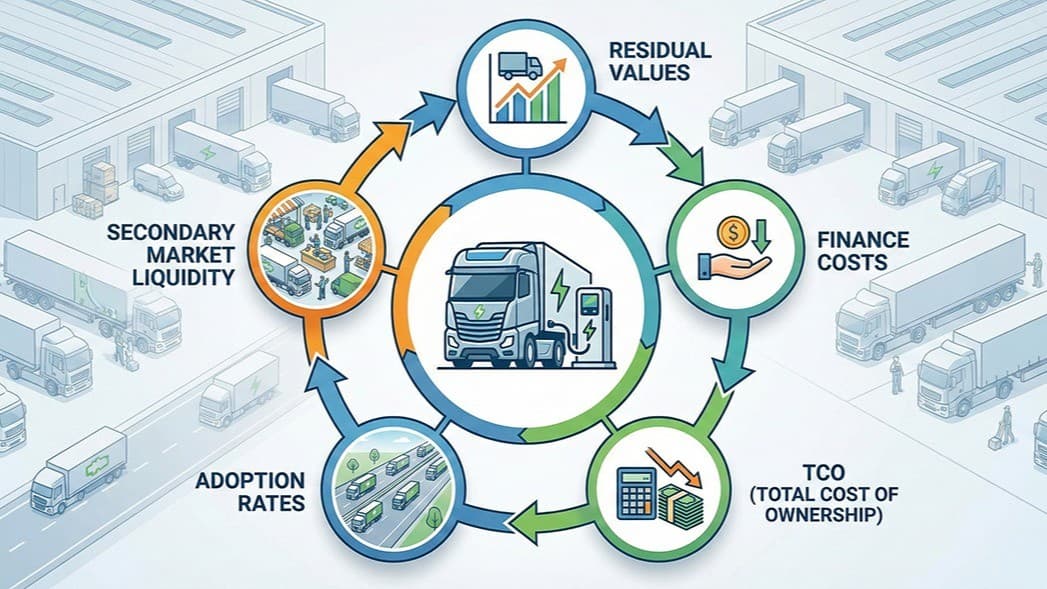

There's a loop at the heart of electric HGV adoption that deserves more attention than it gets.

Residual values affect finance costs → which affect TCO → which affect adoption rates → which affect secondary market liquidity → which affect residual values.

That's not a linear problem with a linear solution. It's a self-reinforcing system with no natural anchor. And it's one of the reasons some eHGV business cases still feel "theoretically compelling, practically fragile".

Right now, fleets are depreciating electric trucks to zero because there's no resale data to justify anything else. Financiers can't price residual risk without transaction history. Operators can't create that history without taking first-mover risk. And the secondary market can't exist without volume and standardisation.

Everyone is pricing risk based on everyone else's uncertainty.

It's a reflexive market in the Soros sense, not a normal supply-demand curve where price discovery happens naturally. The system stays stuck in a low-volume equilibrium: conservative residuals justify high lease costs, high lease costs suppress adoption, low adoption justifies conservative residuals.

Classic negative feedback trap.

The reality is that no single actor can solve this alone. OEMs can't credibly guarantee residuals at scale without massive balance sheet exposure. Policy can't magic liquidity into existence. And operators can't wait forever for someone else to go first.

So what actually breaks these loops?

Three possibilities

Looking at how similar deadlocks have been resolved in other markets, three approaches stand out. None of them is obviously right. All of them raise questions I don't have clean answers to.

1. A balance sheet big enough to eat the risk

Someone acts as residual backstop for long enough that real price discovery can occur. Think less "guarantee" and more "market maker".

In practice, that's either OEM captive finance arms (the Tesla model), state-linked entities (KfW in Germany, potentially UKIB here), or very large fleets effectively self-insuring their residual risk.

The Green Finance Institute and CALSTART are actively developing Residual Value Guarantee frameworks. These are mechanisms where government sets aside reserves to cover the gap between predicted and actual resale values. The economics are compelling: a £10 million reserve could potentially mobilise £250 million in investment, at a fraction of the cost of equivalent upfront subsidies.

But the questions remain: Who in the UK has both the appetite and the mandate to warehouse this uncertainty? Is UKIB the right vehicle? Would Treasury sign off on contingent liabilities for truck residuals? And if the scheme requires funded reserves rather than unfunded guarantees, where does that capital sit on whose balance sheet?

Until someone warehouses that uncertainty, the loop doesn't collapse. But who steps forward first?

2. Artificial liquidity through standards and interoperability

Secondary markets only form when assets are fungible. That means common charging standards, comparable duty cycles, transparent battery health metrics, and transferable warranties.

Without standardisation, every used electric truck is a bespoke science project. No one can price it because no one can compare it.

This is why battery passports, megawatt charging standards, and telematics-driven degradation models matter far more than most policy debates acknowledge. They're not technical features. They're liquidity infrastructure.

The EU Battery Regulation is pushing in this direction. But will the UK follow suit, diverge, or delay? How quickly can state-of-health reporting become standardised enough that a finance house can look at two different trucks from two different OEMs and make a like-for-like residual value assessment?

And here's the harder question: even with perfect standards, does the market have enough volume to create meaningful price signals? Or are we standardising for a secondary market that won't exist for another decade?

3. Asymmetric information collapse

Once enough operators accumulate real-world data on battery degradation, uptime, energy cost stability, and maintenance profiles, the uncertainty band narrows. Residual risk becomes actuarial instead of speculative.

At that point, finance stops being fear-priced and starts being model-priced.

That's the key shift: from narrative risk to statistical risk.

Right now, eHGVs are priced like venture capital. They need to be priced like commercial aircraft. Same physics problem, very different financing regime.

JOLT and the ZEHID programme are generating exactly this kind of operational data. Early results from operators in the field are already showing that real-world performance often exceeds the conservative modelling assumptions. The trucks are going further on less energy than the spreadsheets predicted.

But how much data is enough? How many trucks over how many years before Cap HPI and the finance houses feel confident setting residuals based on evidence rather than anxiety? And who aggregates that data in a way that's credible to the market? OEMs have skin in the game, government programmes have political timelines, and independent operators have no obvious conflict of interest. Each comes with trade-offs.

The regime shift

The reflexivity problem means the market doesn't "gradually transition". It jumps regimes when one of these loops is forcibly broken.

Until then, everyone is rationally waiting for everyone else.

Maybe all three interventions need to happen in parallel: state-backed RVGs to absorb near-term risk, accelerated standardisation to enable fungibility, and sustained data collection to collapse the information asymmetry. Maybe one of them is the obvious lever and I'm overcomplicating it.

I genuinely don't know. But I'm increasingly convinced that talking about eHGV adoption without talking about this financing loop is missing the plot entirely.

The technology works. The operational case is proven. The TCO can stack up.

But none of that matters if the trucks can't be financed at rates that make commercial sense. And they can't be financed sensibly until someone, or some combination of someones, breaks the reflexivity trap.

Who's going to blink first?